Sign in to Your

Ledgible Account

Ledgible Account

If you have an existing account,

please use to the links below to sign in:

please use to the links below to sign in:

Select the Solution Area you're interested in Below:

Click here to read CryptoTax: Events Professionals Ought to Know Part 2

Overstock.com is heralded as the first major retailer to start accepting bitcoin purchases back in January of 2014. Since then several leading e-commerce platforms have followed suit such as Expedia, Shopify, Twitch, and even telecom giant AT&T. Typically these companies will accept cryptocurrency through payment providers such as BitPay, Coinbase Commerce, and others. Amazon does not (yet) offer crypto as a payment option, however, many e-commerce sites will allow you to buy Amazon and other gift cards with crypto which can then be redeemed at your favorite retailer. Paypal has been a payment and withdrawal option for several crypto exchanges for years, but recently rumors have been circulating that the fintech giant may “allow buys and sells of crypto directly from PayPal and Venmo”. (On October 22, 2020 those rumors were confirmed.) Virtual currency such as bitcoin and ether as a means of payment is slowly gaining wider acceptance, but what are the tax ramifications of using crypto as a means of payment for goods and services?Disclaimer: This post is informational only and is not intended as tax or investment advice. For tax or investment advice, please consult a professional.

What Every Tax Professional Ought To Know

Payments company Square, Inc. first allowed Cash App users to purchase and sell bitcoin during the rampant crypto boom of 2017. Since then it has continued to invest in its bitcoin offering, a move that seems to have yielded profitable results!

According to Square’s 2020 Q2 SEC filing, for the six months ended June 30, 2020 and 2019, bitcoin revenue amounted to $1.2 billion and $191 million respectively. The financials indicated that the primary driver behind the soaring 520% increase “was due to growth in the number of active bitcoin customers, as well as growth in customer demand”.

Of course Square is just one of the myriad options available for users to trade crypto today. Coinbase for example, one of the largest and most popular crypto exchanges in the U.S. boasts over 35 million users and over $7 billion in custody.

The majority of crypto users are uninformed when it comes to the potential tax consequences surrounding crypto. Some think that the IRS will not be able to track or trace their trades back to their identity (ouch!).

During 2019 we saw the IRS sending out over 10,000 warning letters to cryptocurrency users to file amended returns if appropriate and pay back taxes. The IRS recently also released the 2020, 1040 draft form, where we can see the virtual currency question has moved from Schedule 1 to near the top of the main form, right under the name and address, asking, “At any time during 2020, did you receive, sell, exchange, or otherwise acquire any financial interest in any virtual currency?”. “Virtual currency” was also included in the 2019–2020 IRS Priority Guidance Plan. These are all unmistakable signals that the IRS is prioritizing crypto.

So, let’s begin with the basics. Selling crypto for fiat (e.g. USD) is a taxable event. The character of the gain or loss depends on whether the crypto is a capital asset (e.g. stocks, bonds, and investment property) in the hands of the taxpayer and the length of time the position was held.

For example, “hodling” (slang in the crypto community for holding the crypto rather than selling it) crypto as a capital asset for longer than a year before selling it will generally result in a long-term capital gain or loss. If the crypto was not held as a capital asset, but rather as inventory for sale in a trade or business, the resulting gain or loss recognized will generally be ordinary in character.

Tools like Ledgible Tax exist to help tax preparers segregate and correctly classify crypto gains and losses. In the world of crypto tax there are many more taxable events than simply selling their crypto for cash. Let’s take a look at some of the other most common transactions in crypto that may result in taxable events.

Disclaimer: This post is informational only and is not intended as tax or investment advice. For tax or investment advice, please consult a professional.

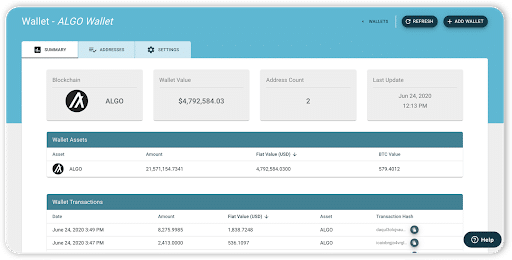

When we first announced the Algorand partnership back in May, we mentioned that the deep integration between Algorand and our Ledgible platform enables us to provide additional services to the Algorand community to meet their growing needs. Today, we’re thrilled to announce that we are offering a special promotion to the entire Algorand community to leverage our Ledgible Tax solution for their individual tax returns.

Tax day (July 15th) is just a few weeks away, and as most everyone knows, the IRS has added a question about your cryptocurrency activity in 2019. If you bought, sold, traded, or received crypto last year, now’s a good time to find a tool to help you figure out your crypto tax liability and file your return.

Tax day (July 15th) is just a few weeks away, and as most everyone knows, the IRS has added a question about your cryptocurrency activity in 2019. If you bought, sold, traded, or received crypto last year, now’s a good time to find a tool to help you figure out your crypto tax liability and file your return.

Ledgible Tax is the latest extension to the most comprehensive cryptocurrency accounting platform on the market. Designed from the ground up for leading CPA firms managing complex cryptocurrency accounting challenges, Ledgible Tax has been recently released to the public for the first time through our Ledgible Tax Partner Program... enabling consumers to get the same enterprise-grade sophistication for their individual tax returns. Offering a wide spectrum of file outputs to facilitate reporting needs, Ledgible Tax supports popular consumer as well as professional Tax preparation systems in addition to standard IRS forms to handle a wide variety of options.

Whether people do their own tax filing or work with a CPA, Ledgible Tax produces the reports they need to account for their crypto activity.

Getting started is as simple as visiting https://tax.fromledgible.com/ and clicking on the “Get Started For Free” button. As the name suggests, it’s completely free to input your wallet and exchange information and get a summary report of your 2019 crypto tax liability. For a small fee, you can download the appropriate report to include with your taxes. For those folks who are coming to the platform through a partner program, like Algorand’s, they can enter a discount code at checkout to receive a limited, one-time discount.

Ledgible Tax includes many of the same features our customers love from Ledgible Accounting and brings them together for a streamlined interface focused on helping users meet the tax reporting requirements triggered by their crypto activity.

Verady will continue to roll out new promotions as part of its Ledgible Tax Partner Program in the coming days as the July 15th tax filing deadline nears. For more information, please contact us at info@ledgible.io or send us a note through the contact form located at: https://ledgible.io/contact/